Businesses Staying in Russia Are Underperforming the Market

Since the beginning of the war in Ukraine, Prof. Jeffrey Sonnenfeld and his team have been tracking which companies have withdrawn from Russia and which are staying put. Their new analysis suggests that the firms cutting ties are seeing markedly better shareholder returns.

A young woman near the Kremlin on April 27, 2022.

This commentary originally appeared in the Washington Post.

A spate of misleading headlines in recent days have harped on the supposed heavy financial costs that companies are bearing for withdrawing from Russia. This has it exactly wrong. Companies that have exited Russia are not only accruing substantial costs; they are also showing financial benefits. And those that refuse to leave are experiencing the greatest costs.

One recent, much-discussed case illustrates this well: Societe Generale’s stock price jumped 5% earlier this month after it announced it was leaving Russia despite incurring a $3.4 billion write-down. This is only the tip of the iceberg.

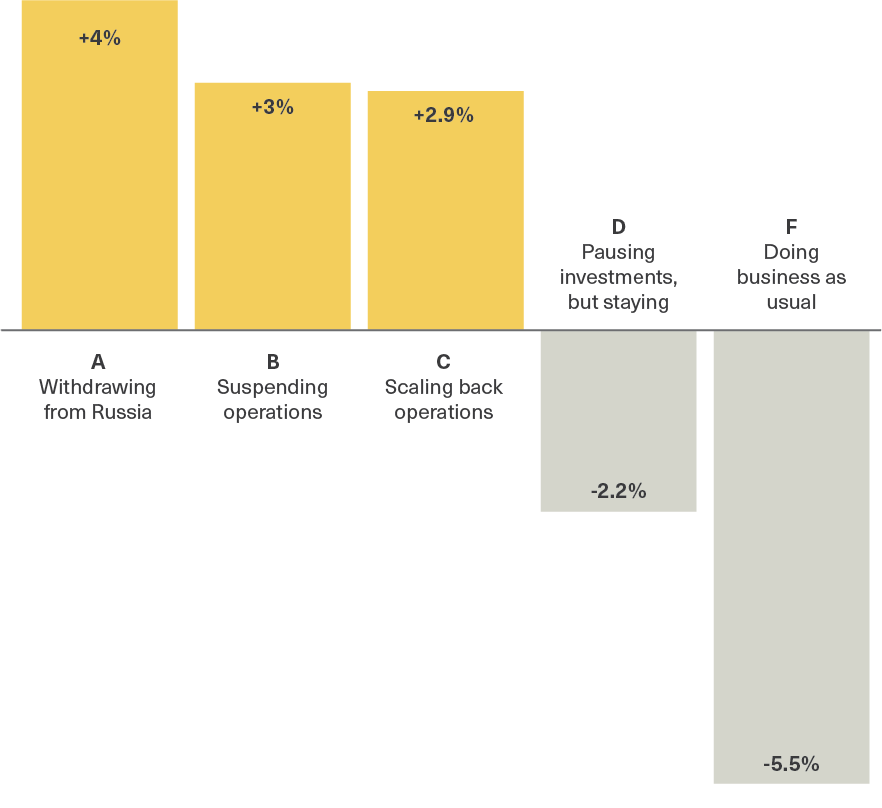

By looking at the market-capitalization-weighted returns of about 600 publicly traded companies, we found that since Russia invaded Ukraine on February 24, companies that curtailed operations in Russia have dramatically outperformed companies that did not over the past two months. Remarkably, the total shareholder returns correspond precisely with the letter grades we assigned companies based on their level of withdrawal from Russia. Those with an A rating—those that have made a clean break or permanent exit from Russia—have performed the best on average, and those with an F rating— those that are “digging in” and defying demand to reduce activities in Russia—are performing the worst.

Impact of the war on companies doing business in Russia

Average market-capitalization-weighted returns from February 23 to April 8

We have been maintaining an authoritative list tracking the responses of more than 1,000 global companies since the invasion of Ukraine began. As soon as our list appeared on CNBC two months ago, many of the companies we identified as remaining in Russia saw their stocks plummet 15 to 30%, even though key market indexes fell only about 2 to 3%.

We noticed the same trend play out over time, amplified by the release of investment research reports based on our list. That’s why our financial and economic researchers, led by Steven Zaslavsky, Yash Bhansali, and Ryan Vakil, used our proprietary database to examine this phenomena. The findings confirm that financial markets are strongly rewarding companies that withdraw while punishing those that remain.

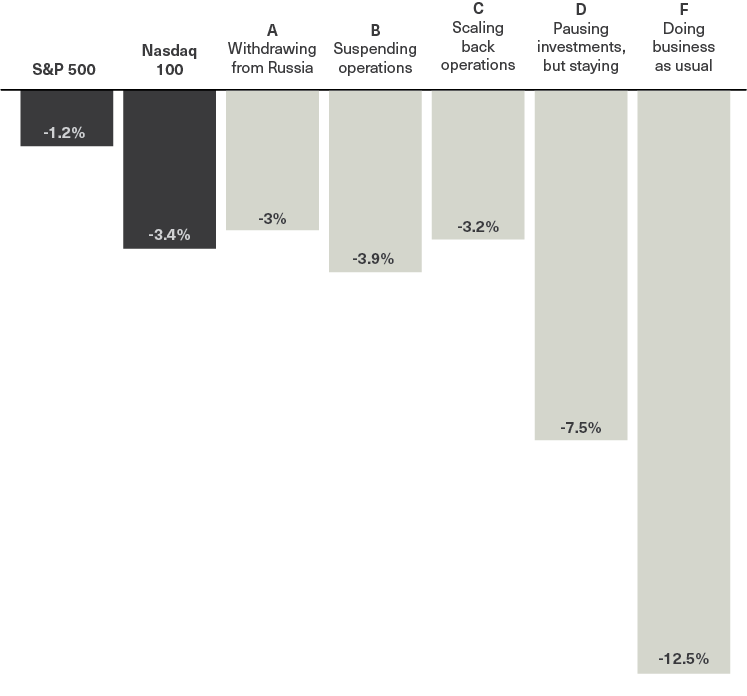

The strong response from markets was particularly pronounced in the initial weeks following the invasion. Companies that curtailed operations to some degree over the first three weeks generally tracked the broader market sell-off of about 3 percent across major market indices, while companies that refused to withdraw were down a startling 7.54% for those with a D rating and 12.54% for those with an F rating.

Widespread loss in the initial weeks

Market-capitalization-weighted returns from February 23 to March 11

Further analysis reveals that this pattern of outperformance by companies that withdrew held true across multiple factors, including the regions and sectors of the companies included. We saw the trend remained consistent even across different market capitalization segments, suggesting that even smaller, less well-known companies that remained in Russia were not immune to strong investor backlash.

Even smaller companies that remained in Russia saw investor backlash

| A—Withdrawing from Russia | F—Doing business as usual | |

| Small cap | +6.5% | -12.2% |

| Mid cap | -2% | -7.8% |

| Large cap | +4.2% | -5.3% |

Some have suggested that companies that draw large proportions of their revenue from Russia might be more hesitant to leave Russia or that these Russian-reliant companies would suffer more financially, yet our research shows that companies that draw upward of 5 percent of revenue from Russia have not differed in total returns from those that draw less.

Indeed, many of the companies that are most reliant on Russian revenue are commodity producers that have been more than offset by rising global commodity prices. For example, ExxonMobil stock has increased by 13% since the invasion despite writing off billions in Russian assets and forswearing its profitable Russian operations. Meanwhile, Kinross Gold has gone up by 13% even though it exited its investment in the Russian Kupol gold mine, which accounted for 20% of its revenue. Even BP, which took a hefty $25 billion hit by writing down its holdings in Rosneft, is in the green.

Thus, contrary to media narratives, when it comes to companies exiting Russia, the focus should not be on their lost revenue or the assets they had to write off. Russian revenue makes up a small percentage of most companies’ revenue. And even for the multinational companies that previously drew significant revenue from Russia, investors are clearly much more concerned with the far more important reputational risk of funding the Putin regime and with the potential for large-scale corporate boycotts around the world.

In other words, the far more dangerous financial threat to shareholders is remaining in Russia—not writing off Russian assets. Those companies that have stayed their course should take note.